Notice of Assessment

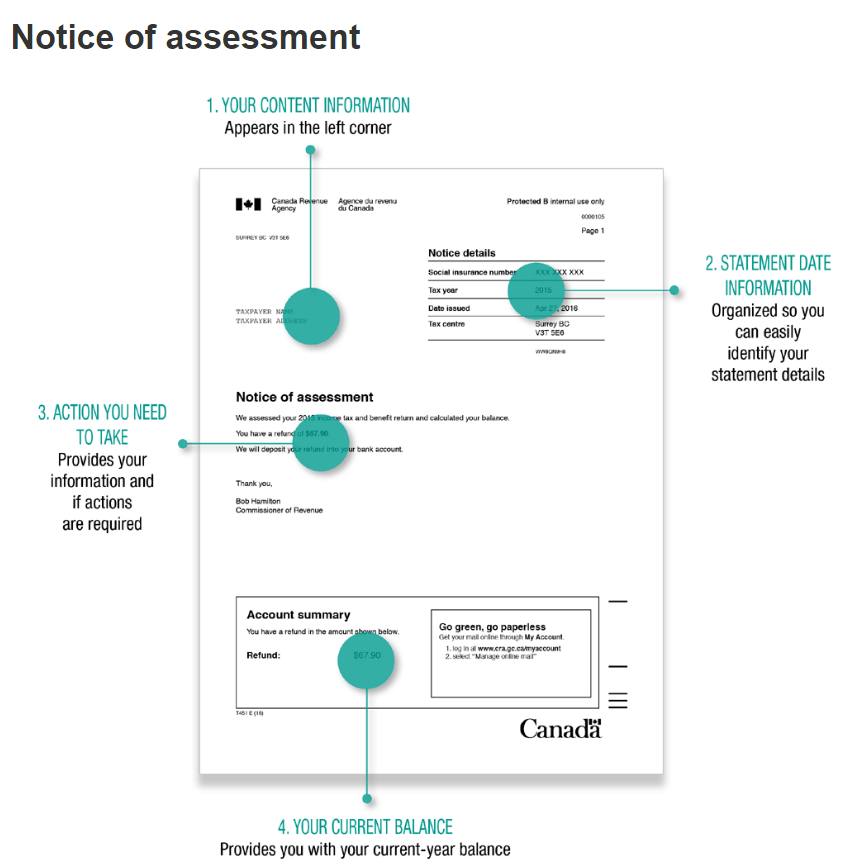

The Notice of Assessment (NOA) is produced by Canada Revenue Agency after you have submitted your annual tax filing. It confirms that they have assessed your tax return and acts as validation that your income tax return numbers were correct and truthfully stated.

You will receive your Notice of Assessment by mail from CRA after your tax return has been assessed. The printed and mailed version looks like this:

Online Access to your Notice of Assessment

You can also reprint your NOA online using the CRA My Account service.

To print a Notice Of Assessment from CRA My Account online, follow the steps below:

1. Login to CRA (http://www.cra-arc.gc.ca/myaccount/)

2. From the Overview page, click the menu link for ” Tax returns ”

3. In the row for the desired Tax year, click the “Notice of assessment” link

4. The Notice of Assessment will appear as a single long page. Verify that it shows the correct “Tax year” that your broker has requested. Then click the “Print/Save” link at the top right of the document.

5. Make sure you print or save all pages.

6. If your Notice of Assessment states that you need to pay an amount (i.e you have a balance due for your most recent tax year, showing as a DR amount at the bottom of your NOA), please also print your CRA Statement of Account to show the balance has been paid. You can find instructions for printing your CRA Statement of Account here.

Open Mortgage

A mortgage which can be prepaid at any time, without penalty. Interest rates are usually higher for open mortgages.

Pay Statement

A pay statement (often referred to as a pay stub) is the form you receive each pay period you work. The pay statement should confirm your gross income amount over the pay period, and lists any deductions your employer holds back for taxes and insurance, etc. to result in the “Net Pay” that you receive. The pay statement also includes Year To Date (YTD) amounts for your gross pay and deductions taken.

For a pay statement to be acceptable to a lender, it must show

- employer name or logo (usually in the header or footer area)

- the client name

- a clear breakdown of your gross pay for the period (including hours if your position is hourly), deductions and net pay

- your Year To Date (YTD) amounts.

Here is an example of a typical pay statement from an employer that uses a 3rd party payroll services provider (ADP, Ceridian, etc):

Example Pay Statement – Payroll Services

Here is another example of a Pay Statement issued by a company that uses an internal accounting/payroll software (Simply Accounting) to issue printed cheques:

Example Pay Statement – Simply Accounting

DND Personnel

DND personnel receive slightly different pay statements (a mid month and an end of month statement). At the beginning of the month you receive a ‘mid month’ statement that shows your full monthly salary, all deductions, the amount to be deposited at mid month, and then a holding amount which will be deposited at the end of the month. For DND clients, the lender will want the MID MONTH statement, which looks like this:

Example Pay Statement – DND Mid month

Payment Frequency

How often you want to make payments: every week, every other week, twice a month or monthly.

Porting

This means that you can take your mortgage with you to another qualifying property without having to lose your existing interest rate and avoid prepayment penalties.

Prepayment Charge

A fee charged by the lender when the borrower prepays any part of a closed mortgage beyond what is allowed in prepayment privileges set out in the mortgage agreement.

Prepayment Privileges

Mortgages usually include some prepayment privileges which give you the right to pay some extra money towards your principal and thus reduce the amount of interest you’ll pay in the future.

For example, some lenders allow prepayment of up to 20% of the original mortgage balance per year through lump sum payments (can happen any time throughout the year) or you can increase the regular scheduled payments by up to 20% (the extra going straight to your principal).

These privileges are different for each lender and sometimes for different mortgage products, so you always want to ask for an explanation of the mortgage prepayment privileges when you are comparing different mortgage options. Often mortgage products that have the lowest rates will have reduced privileges as a tradeoff.

Principal

The amount of money borrowed for a new mortgage.

Principal, Interest, Taxes (P.I.T.)

Principal, interest and taxes. These make up the regular payment on a mortgage if the lender is including property taxes in your mortgage payments.